Diminished Value Frequently Asked Questions:

1. Will my damaged vehicle ever be the same as before?

This would depend greatly upon the nature and severity of the damages sustained and the manner and quality of the repair performed as well as the vehicle itself and history of prior damages etc. Minor damages such as merely a damaged tail light or chrome bumper may be properly replaced with factory replacement parts whereas little if, any evidence of repair would be found even by the most experienced professional.

A vehicle which has sustained major damages, even after receiving the best possible repair, will not only have a history of being damaged but most often will have remaining signs of repair which will be easily noticed by a professional (i.e. car dealer at trade in, post repair inspector, potential buyer etc.). Such remaining indicators will cause a loss in value and may pose remaining safety related flaws and defects as well.

2. How much value has my vehicle lost due to its recent accident.

The loss in value of a damaged vehicle is known as Diminished Value. The amount of Diminished Value of a damaged and repaired vehicle depends upon several factors including: the pre-loss value of the vehicle, the nature and severity of the damages and the cost, manner and thoroughness of the performed repairs.

Consider that, when a vehicle is in an accident, it loses its greatest value just after the actual impact or occurrence. During the dismantling, repair, installation and painting of replacement parts, the value is slowly restored as the repairs progress.

The full original value will likely never be regained simply because the vehicle now has a history of damage that it did not have before the loss. Prior damage history will be disclosed to potential buyers who will likely not pay the same for a vehicle with a damage history as compared to one with no damage history. This is often referred to as “the damaged goods syndrome”.

If the repairs are done thoroughly and in a workmanlike manner, the value of the vehicle can be maximized to the best of reasonable human ability but likely never to its pre-loss value.

If the repairs are done to less than thorough and workmanlike standards, the recovery in value will be limited accordingly, and the vehicle will suffer a greater loss or diminishment in value.

The more significant the damages, the greater the loss in value. The poorer the repair quality, the less recovery of the vehicle’s original and pre-loss value.

In order to make this determination you should secure the services of an independent professional to perform a visual inspection of the vehicle and prepare an expert assessment of your remaining loss.

3. How will damage history affect my trade-in or the sale of my vehicle?

Under most state laws, every auto dealer is to disclose an accident history on a vehicle to a potential buyer. To be in compliance, and avoid lawsuits, they are often careful to ask regarding the damage history from the prior owner and may even have the owner sign an affidavit. After disclosure, most buyers are not willing to pay the same amount for a vehicle with an accident history as they would for the same vehicle without an accident history.

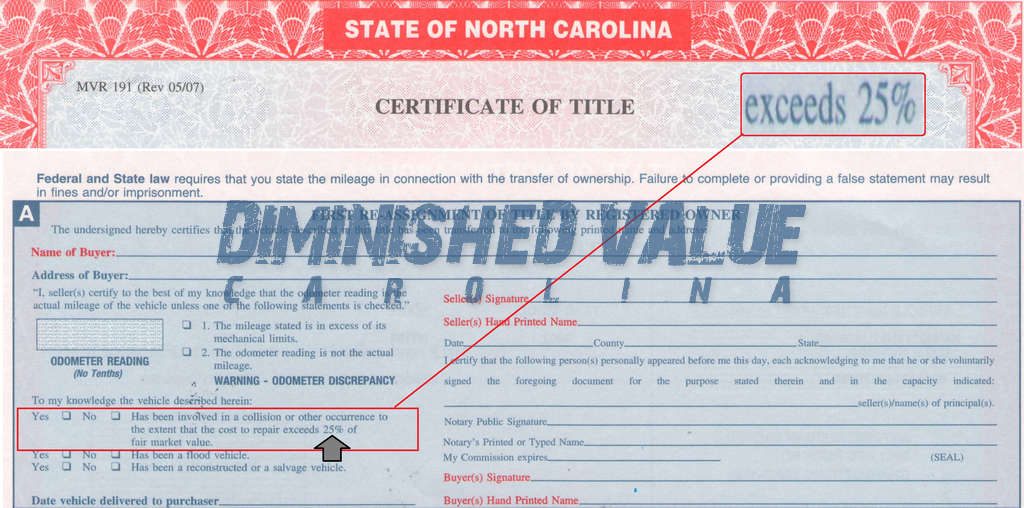

4. What is Loss of Value or Diminished Value?

Loss of Value or Diminished Value is the difference in the market value of a vehicle without an accident history and the market value of the same vehicle with accident history. Unlike depreciation, which is an anticipated and predictable loss in value incurred over time, Diminished Value is an unexpected and sudden loss in value due to a specific occurrence. This loss may be recovered as part of a property damage claim.

5. What about Internet based Evaluations of my loss in value?

First of all, the most important and easily overlooked aspect of performing a proper and thorough Diminished Value Assessment is the manner and thoroughness of the actual repairs performed. This is why Internet based evaluations without actual vehicle inspections are not considered to be accurate or recommended by respected industry professionals or likely to be admissible as evidence if needed. A comprehensive and accurate Diminished Value inspection will provide a two or three-dimensional approach whereas the site-unseen Internet valuations are merely one dimensional.

Secondly, these sight unseen Internet valuations do not provide an unbiased valuation of the vehicle’s pre-loss condition which is one of the fundamental basics required to perform an accurate diminished value assessment. It would compare to your purchasing a vehicle sight un-seen.

These Internet based reports provide only an estimated valuation of the Inherent Loss in Value and provides no source to evaluate the manner, thoroughness or quality of the performed repairs and parts nor any further loss in value resulting from same.

Without physically inspecting the vehicle it would be impossible to evaluate the performance of both the insurer (Insurance Related Diminished Value) and/or repairer (Repair Related Diminished Value) in the repair of the vehicle, and one would likely not receive full compensation for their full remaining loss.

Thirdly, many of these Internet Diminished Valuation services utilize what is known as the “Georgia” or “17C Formula”. This formula was developed by insurers and originally adopted by the State Of Georgia as one means of attaining a value after Georgia adopted the premise that Diminished Value could be claimed by first party insured’s. However, as this formula was contested by consumer advocates the state agreed that the formula was not accurate and they promptly divested themselves from endorsing the formula. Many insurers continue to attempt to utilize this formula in their settlement offers despite the State Of Georgia’s change in position. While Internet based DV assessments may be less costly, you may not get the full scope of your damage and repair thus one may lose significantly more than one might save.

More importantly, there is no physical inspection of the repaired vehicle to determine if serious safety related issues may be present and remain in need of correction.

Consider the fact that during the manufacture of a vehicle there is an average of 600 visual inspections during the manufacturing process. Wouldn’t it make sense that after re-construction from accident related damages that at least one visual inspection would be prudent?

6. What am I owed after an accident?

As a result of damages sustained in a covered loss and a claim made against an insurer, the insurer is obligated to provide for either the repair or replacement of the damaged property.

Normally the insurer is given the authority to make the decision to either repair or replace the damaged property. Once they make the decision they are held to a level of “pre-loss” condition and/or “actual cash value” (ACV).

Should the insurer elect to repair a damaged vehicle, they owe the costs to restore the damaged vehicle to its pre-loss condition to the best of reasonable, human ability.

Should the insurer elect to deem the damaged vehicle to be a total-loss, they are obligated to provide replacement or actual cash value enabling the claimant to purchase another vehicle equal to the value of the damaged vehicle, immediately prior to the loss. The rules of indemnification are clear in as much as what is owed is what was possessed just prior to the loss, no better and no worse.

Additionally, you may be entitled to sales tax, tag and title transfer costs in the event your vehicle is determined to be a total loss.

You may be entitled to ‘loss of use’ (temporary substitute vehicle) during the time required to make repair; or, seek a replacement vehicle from the at-fault party, their insurer, or as may be provided by coverage within your personal insurance policy.

7. Who is responsible to pay?

If you make a claim against your own insurer it is considered a first party claim and you will be dealing with your insurance company based on the terms and conditions as outlined within your insurance (contract) policy.

If the accident was someone else’s fault and you are making a claim against them through their insurer, it is considered a third party claim. You are under no contractual obligation to let the other person’s insurance company inspect the damages or determine the extent of damages or cost of repair. You may, if desired, secure repairs and merely submit a bill to the at-fault party and/or their insurer for reimbursement. The at-fault party’s insurer will likely provide for your damages based upon the ‘limits of liability’ coverage under the at-fault party’s insurance policy.

It’s important to understand that the at-fault party owes you for your damages and while their insurer owes them under the terms of the property damage portion of their policy contract, the at-fault party’s insurer legally owes you, the victim, nothing. The insurer will normally attempt to settle the claim on behalf of their insured as is owed to their policyholder under the terms of their insurance policy.

8. How do I recover all my losses?

The key to recovering all losses owed is to know just what it is that is owed you. Having an in depth visual inspection of the damaged/repaired vehicle and accurate assessment of your remaining damages prepared for you and understanding the necessary steps in the recovery process in paramount. Providing a detailed report with your claim will enable the insurer a clear understanding of your remaining loss and facilitate a more timely settlement.

9. Can I disagree with the amount of loss?

YES. Vehicle owners have the right to disagree with any assessed amount of loss. Depending on the policy and state law, provisions are provided for dispute resolution. Of course before one can make a determination if the insurer’s offer is reasonable or not, they will need a valuation of there own for comparison.

10. How do I know all repairs were completed properly?

It is important to completely inspect the vehicle when it is delivered but often the average consumer cannot see all remaining damages, flaws and defects. If you are unsure we strongly suggest you hire an independent appraiser to perform a post repair inspection – any flaws or defects in repairs after an accident or “evidence of repairs” can negatively affect your trade-in or resale value. Remaining safety related issues may also go unnoticed and uncorrected placing occupants and others on the roadway in possible jeopardy.

11. Who is working for me… the repairer or the insurer?

The consumer is usually pitted between the insurance company’s need to minimize their losses and the repair facilities need to make a profit. Today many repair facilities and insurance companies have established mutual relationships similar to a HMO/PPO referred to as “DRP” or “Direct Repair Programs” whereas the repairers adhere to insurer mandates in exchange for continued referrals. These mandates are to keep repair costs low and may restrict proper repair techniques, materials and processes. Far too often these DRP relationships have the repair shop working for the insurer and not you or in your best interests. In most cases it is best to seek a truly independent repairer, of your own selection, (based upon recommendations from those you know and trust) who will work for you in the proper restoration of your vehicle. If it is a DRP shop than ensure that they understand it is you whom they work for in the repair of your vehicle. If needed, get it in writing! Most state laws mandate that the choice of repairer is yours and yours alone. Don’t trust others to make such important decisions with your economic and personal welfare.

The consumer may need an unbiased third party Professional Expert to assure that such circumstances do not short change them in the recovery of their losses owed them under their policy and/or the law. Ask us about our services in pre-repair assessments, in-process repair monitoring and post repair inspections.

12. Should my car be totaled?

Determining if a vehicle should be repaired or not depends on the economic factors surrounding the claim as well as state mandates and regulations designed to protect consumers.

As a general rule, when the damages meet or exceed 80% of the damaged vehicle’s pre-loss market value the vehicle will be considered a total loss. Insurers may elect to total a vehicle prior to reaching this percentage and it is rare that they would exceed it.

The insurer is given the liberty to make the decision to repair or replace (within state laws and guidelines) and once determined, the insurer is held to certain standards in their performance of their selected option. In either option, the consumer is to be indemnified for their loss and placed as closely as possible to the economic position they were just prior to the loss.

13. What should I expect from the insurer?

Based upon past case history, the court has stated that an insurance claims adjuster has no affirmative obligation to advise an insured or third party claimant of their rightful entitlements; however when an adjuster provides information to a claimant about the claim, the adjuster must be truthful. As “Buyer Beware” is aged and sound advice for a buyer, the same adage may be appropriate for exercising caution when one is making a claim against an insurer.

14. Does my ability to recover Diminished Value depend on who was at- fault?

Your ability to recover Diminshed Value may depend on who was at fault, depending on various factors. There are two entirely different grounds for recovering the loss in value which apply depending on your status as either a first party or a third party claimant. First parties are usually seeking recovery of their damages from their own insurance company, whether the insurer pays for Diminished Value depends upon the terms of the insurance policy and the state’s interpretation of that policy and perhaps the insurer’s activities during the claim process. Third parties usually seek damages from the at-fault driver and/or their insurer for the loss in value as part of the property damages caused by the negligent driver. Most states allow for such recovery against the negligent party under what is known as ‘Reinstatement of Torts’.

15. My state is a “No-Fault” state. Does that make a difference?

The term “No-Fault” generally refers to claims for injury and not necessarily property damage issues. In most states the “Reinstatement of Torts” is the rule followed whereas the at-fault party is responsible for all financial damages caused to another resulting from their negligence which may include Diminished Value.

16. What should I do if I am involved in an accident?

No matter how minor, it is wise to report every accident to the police. Then, contact the collision repair shop of your choice. Your independent collision repair shop can assist you with the processing of your claim, answer your questions, and advise you to ensure safe and proper repairs are made to your vehicle restoring as much value as humanly possible.

17. Do I have to take my vehicle to a drive-in claims center or get multiple appraisals?

No. If you request it, your insurer must inspect the damage to your vehicle at your chosen collision repair shop rather than at their drive-in claims center. They are legally prohibited from coercing or using any tactics intended to prevent you from seeking damage appraisals from your own body shop rather than their drive-in facility.

18. Do I have to use a specific collision repair facility?

No. In most states, including Florida and Oregon, you have the absolute right to select the collision repair facility of your choice. If the insurer gives you a list of ‘recommended repair shops’, they likely will have indicated repair shops which have entered into a contract with them. These shops may see the insurer as their customer, not you, the vehicle owner. These agreements may determine how your vehicle will be repaired and may encourage the use of non-original aftermarket replacement parts or call for shortcuts and other cost saving activities. By choosing an insurance preferred or referral shop, you may be giving up your rights in the proper and thorough repair process.

19. What is “Steering”?

Steering is the act of directing a insured and/or claimant to, or away from, any specific repair shop or requiring that repairs be made by a specific repair shop or individual. Steering by insurance companies can be subtle to extremely aggressive and is considered an unlawful practice in Florida.

20. How do I know if I am being steered?

If you are told that; “It will take longer to get your car repaired” or “cost more if you choose your own shop”, BEWARE. You are probably being steered. Statements such as “You’ll have to pay the difference out of pocket”, “We won’t guarantee the work if you take the car there,” or “We won’t pay the difference” are misleading and intended to scare your into taking your vehicle to a repairer of the insurer’s choosing. The choice of repairer is yours, use it wisely!

Most states, including Florida and Oregon, have consumer protection laws that require insurance companies to expedite appraisals within specific time frames. Insurance companies are required to perform accurate investigations and assessment of damage and to negotiate in good faith with any collision repair facility on the proper cost to repair the vehicle to pre-accident condition. You pay insurance premiums and contract to pay a specific deductible in the event repairs are required. In effect, you’ve already paid for proper repairs. Don’t be intimidated. Steering is illegal in Florida and Oregon

21. Why should I choose my own collision repair facility rather than one “suggested” by the insurance company?

There are compelling reasons to choose an independent, trusted repair shop that you know will make sure the vehicle is truly restored to its pre-accident condition to the best of human ability. Insurance appraisers work for the insurance company. Truly independent auto collision repair facilities work for you. They are looking out for your best interest. They will negotiate directly with the insurance company for the proper repairs on your behalf so that your vehicle is safe for you and your family. Independent collision repairers look out for your best interests and will serve as your advocate during the repair process.

‘Preferred’ or ‘Direct Referral repair shops’ represent the insurance company in both negotiations and the repair of the vehicle. They contract with insurance companies regarding the repairs, the costs and the repair procedures in exchange for the insurer having damaged vehicles steered to them. The insurance company sets the rules and the repair shop simply follows them to keep the insurance companies sending them work. Better is never cheaper and cheaper is never better! These “relationships” between the insurer and repairer may affect the quality and thoroughness of the repair service and/or the quality and condition of the parts used. You have paid your insurance premiums with the expectation of receiving safe and proper repairs that truly restores your vehicle to its pre-loss condition to the best of human ability. Make sure you get what your entitled.

22. What are imitation or non-OEM parts?

Imitation parts (a.k.a. generic, aftermarket, ‘quality replacement’ or non-original equipment manufacturer (non-OEM), ‘Taiwan Tin’, ‘Off-shore sheet metal’, ‘Counterfeit’, etc) are “knock-off” copied parts made by a company other than the manufacturer of your vehicle. These parts are made to look like your vehicle’s parts, but have likely never have been crash tested and are not covered under your vehicle manufacturer’s warranty for fit, finish or function. In its February 1999 issue, Consumer Reports published the results of its extensive study of non-OEM parts. The cover story was entitled, “Shoddy Auto Parts: How to beat car repair rip-offs, Bumpers that shatter, Parts that don’t fit, Fenders that rust”.

In addition to these concerns, there are no provisions for recalls based on the safety or performance (or lack thereof) of these parts. Your insurance company may attempt to use imitation parts to save money on your vehicle’s repair. An independent collision repair facility will help you negotiate with your insurance company for the appropriate originalequipment manufacturer’s parts to maintain the integrity and value of your vehicle and safety of you and your family.

23. Who guarantees the workmanship for the repairs?

The repair facility is responsible for the workmanship. Insurance companies do not repair automobiles therefore they cannot extend warranties for repairs. If there is a concern, even with a facility selected by the insurance company, the facility itself is responsible. Ask your local independent repair facility for their warranty, in writing.